The State Bank of Pakistan (SBP) on Monday decided to keep its benchmark policy rate unchanged at 11.5%, citing persistent inflationary pressures, uncertainty arising from the US-Iran conflict, and a broadly unchanged macroeconomic outlook. The decision was announced following a meeting of the Monetary Policy Committee (MPC), which noted that while global oil prices had eased after recent positive geopolitical developments, they remained significantly above pre-conflict levels and continued to pose risks to inflation.

Inflation Trends

The central bank reported that inflation had accelerated sharply in recent months, with headline inflation rising from 7.3% in March to 10.9% in April and further to 11.7% in May. Core inflation also edged higher, reaching 8.7% in May from 8.2% a month earlier, reflecting the broader impact of higher energy and transportation costs on the economy. The MPC assessed that the current monetary policy stance remains appropriate to guide inflation towards the target range of 5-7% over the medium term.

Impact of Middle East Conflict

The committee observed that the economic consequences of the prolonged Middle East conflict, which it had anticipated during the previous policy meeting, were now becoming visible in key economic indicators. According to the SBP, inflation has been driven not only by higher domestic energy prices linked to global oil market disruptions but also by rising production and transportation costs. Additionally, an unexpected increase in wheat and wheat-related product prices significantly pushed up food inflation during April and May.

The central bank warned that inflation could remain in double digits over the coming months before gradually easing. However, it highlighted several risks to the outlook, including geopolitical developments, adjustments in fuel, electricity and gas prices, fiscal slippages, and weather-related pressures on food supplies.

Economic Activity

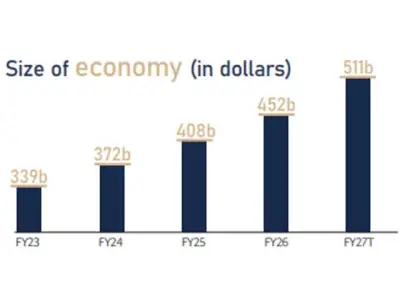

Despite rising inflation, the MPC noted signs of moderation in economic activity. Elevated prices, fiscal austerity measures, and prevailing uncertainty were weighing on business activity and consumer spending. The committee pointed to provisional estimates released by the Pakistan Bureau of Statistics (PBS), which showed that the economy grew by 3.7% in FY26 compared with 3.2% in FY25. However, the MPC noted that growth would likely have been stronger had it not been for the impact of the Middle East conflict and ongoing fiscal tightening.

The growth performance was mainly supported by the services and industrial sectors, while agriculture also contributed positively. Large-scale manufacturing expanded by 6.5% during July-March FY26, although the central bank expects growth in the sector to slow in the final quarter of the fiscal year. Looking ahead, the MPC warned that spillover effects from the regional conflict could continue to dampen industrial and services sector activity. At the same time, subdued agricultural prospects due to challenging weather conditions and uncertainty surrounding Kharif crops may affect growth during FY27.

External Sector

On the external front, the central bank described pressures as manageable despite a deterioration in the current account during April. The current account posted a deficit of $0.3 billion in April, resulting in a cumulative deficit of $0.2 billion during July-April FY26. The deterioration was largely attributed to a widening trade deficit caused by higher energy imports, although robust workers' remittances continued to provide support. The MPC said strong remittance inflows in May were expected to help contain the current account deficit for FY26 near the lower end of earlier projections.

Pakistan's external position also benefited from increased official inflows following the successful completion of reviews under the International Monetary Fund's Extended Fund Facility (EFF) and Resilience and Sustainability Facility (RSF). As a result, the SBP's foreign exchange reserves rose to $17.2 billion as of June 5 and are projected to reach $18 billion by the end of June. The committee expressed confidence that reserve accumulation would continue in FY27 through ongoing foreign exchange purchases and planned official financing.

Fiscal Position

On the fiscal side, the MPC observed that the government's consolidation efforts remained broadly on track, primarily due to expenditure restraint. While revenue growth slowed during July-March FY26, the government revised the Federal Board of Revenue's (FBR) collection target to around Rs13 trillion and still expects to achieve a primary surplus of 2.5% of GDP this fiscal year. For FY27, the government has set a primary surplus target of 2% of GDP.

The MPC stressed the importance of maintaining fiscal discipline and accelerating structural reforms, particularly measures aimed at broadening the tax base and reforming public sector enterprises. The committee also highlighted continued growth in private sector credit, which expanded by around 13%, reflecting increased borrowing for working capital, investment, and consumer financing.

Reaffirming its commitment to price stability, the central bank said it would continue to closely monitor economic developments and adjust policy as necessary while urging faster implementation of structural reforms to strengthen economic resilience and support sustainable growth.